Monday, February 29, 2016

qotd: Physicians & Medical Students: Sign the open letter on the truth about Medicare-for-All

The Huffington Post

February 28, 2016

Setting the Record Straight on Medicare for All: An Open Letter From 560

Physicians and Medical Students

By Steffie Woolhandler and David Himmelstein

/The following statement has been signed by more than 560 physicians and

medical students. It was crafted by Andrea Christopher, M.D., Fellow in

General Internal Medicine at Harvard Medical School, Adam Gaffney, M.D.,

Fellow in Pulmonary and Critical Care Medicine at Massachusetts General

Hospital and Harvard Medical School, and the two of us, Drs. Steffie

Woolhandler and David U. Himmelstein. Other physicians and medical

students are invited to read and sign the statement here:

//medicare-for-all.us/ <http://medicare-for-all.us/>

*Setting the Record Straight on Medicare for All: An Open Letter From

560 Physicians and Medical Students*

The renewed debate over the merits of single-payer health reform has

been marred by misleading claims that such reform is unnecessary and

unaffordable. We write to set the record straight.

Despite the advances of the Affordable Care Act (ACA), the health care

financing system continues to inflict needless suffering on our

patients. Nearly 30 million Americans remain uninsured, and co-payments,

deductibles and insurers' narrow networks obstruct care for many more.

Insurers skim billions from premiums, and impose expensive and

time-consuming paperwork on doctors, nurses and hospitals.

Studies in the most trusted journals have quantified the bureaucratic

savings achievable through single payer reform. We devote31 percent of

medical spending to administration, vs. 16.7 percent in Canada

<http://www.nejm.org/doi/pdf/10.1056/NEJMsa022033> - a difference of

$350 billion annually. And single-payer systems in Canada, the UK and

Australia all use their bargaining clout to get discounts of 50 percent

<http://content.healthaffairs.org/content/32/4/753.abstract> from the

prices drug companies charge our patients. The potential savings on

bureaucracy and drugs are enough to cover the uninsured, and to upgrade

coverage for all Americans - a conclusion affirmed over decades by

multiple analysts <http://www.pnhp.org/facts/single-payer-system-cost>,

including the Congressional Budget Office and the Government

Accountability Office.

Recent critics of Medicare for All warn of large increases in government

spending, but fail to note

<http://www.huffingtonpost.com/david-himmelstein/kenneth-thorpe-bernie-sanders-single-payer_b_9113192.html>

that these would be fully offset by savings on private insurance

premiums and out-of-pocket costs. Their forecasts of massive surges in

doctor visits and hospital care conflicts with past experience of

coverage expansions. When 15 million Americans gained insurance under

the ACA in 2014, hospital admissions

<http://www.aha.org/research/rc/stat-studies/fast-facts.shtml> didn't

budge <http://www.aha.org/research/reports/tw/chartbook/ch3.shtml>. No

surge in hospital use

<https://www.census.gov/library/publications/1975/compendia/hist_stats_colonial-1970.html>

or doctor

<http://www2.census.gov/library/publications/1975/compendia/hist_stats_colonial-1970/hist_stats_colonial-1970p1-chB.pdf>

visits

<http://www2.census.gov/library/publications/1968/compendia/statab/89ed/1968-02.pdf>

occurred when Medicare and Medicaid were rolled out, or when Canada's

single-payer system started up

<http://www.nejm.org/doi/full/10.1056/NEJM197311292892206>; doctors saw

sick and poor patients more often, but their healthy, wealthy patients a

bit less often.

Experience in many nations over many decades

<http://stats.oecd.org/index.aspx?DataSetCode=HEALTH_STAT> provides

convincing evidence that single-payer reform is both medically necessary

and economically advisable.

/In addition to Drs. Gaffney, Himmelstein, Christopher and Woolhandler,

this statement has been signed by //more than 560 other/

<http://medicare-for-all.us/endorsers/>/physicians and medical students./

http://www.huffingtonpost.com/steffie-woolhandler/setting-the-record-straig_24_b_9341782.html

***

Comment by Don McCanne

With the recent often inaccurate and ill-advised debate taking place in

the media over the financing of single payer it is imperative that the

record be set straight on the basic, irrefutable facts of single payer.

Physicians and medical students who are well informed on the true facts

should sign this open letter so that the nation understands clearly that

we can ensure that absolutely everyone has free choice of health care in

a system that is affordable for everyone, through an improved

Medicare-for-All.

Go to /medicare-for-all.us <http://medicare-for-all.us>/to sign the letter.

Colleagues should be encouraged to sign as well. Non-physicians are also

encouraged to endorse this letter by signing on to a companion list at

this same website.

In a separate release, Steffie Woolhandler explains the background that

makes this action an imperative:

"The recent attacks on single payer reform by some liberal economists

and politicians are mystifying. When I met with Hillary Clinton some

years ago she acknowledged that single payer would be the cheapest and

most efficient way to cover all Americans. Her only objection then was

that single payer wasn't politically feasible. Now she's charging that

the numbers don't add up. And economists who once projected large

savings from single payer, are now saying the opposite, without citing

any new data. They're playing political games at the expense of the

truth."

Again, please go immediately to /medicare-for-all.us

<http://medicare-for-all.us> /to sign the open letter.

Friday, February 26, 2016

qotd: AP-GfK poll on single payer spreads falsehoods

AP GfK

February 25, 2016

AP-GfK Poll: Support shaky for Sanders 'Medicare for all'

By Ricardo Alonso-Zaldivar and Emily Swanson

At first blush, many Americans like the idea of "Medicare for all," the

government-run health system that's a rallying cry for Democratic

presidential candidate Bernie Sanders.

But mention some of the trade-offs — from higher taxes to giving up

employer coverage — and support starts to shrivel.

That's the key insight from an Associated Press-GfK poll released

Thursday. The survey also found that people's initial impressions of

Sanders' single-payer plan are more favorable than their views of

President Barack Obama's health care overhaul.

A slim plurality of 39 percent supports replacing the private health

insurance system with a single government-run, taxpayer-funded plan that

would cover medical, dental, vision and long-term care, with 33 percent

opposed. Only 26 percent say they support Obama's hard-won health care law.

Asked whether they would continue to support Sanders' plan if their own

taxes went up, under a third of initial supporters of the plan would

keep backing it. About 4 out of 10 flipped to opposition.

About the same share of initial backers would ditch single-payer if it

meant that people had to give up employer coverage. Twenty-eight percent

would continue to support it.

Higher taxes and an end to employer coverage are both a given under the

Sanders plan, which would replace private coverage with a

taxpayer-funded program, while also offering more generous benefits such

as no deductibles and no copayments, as well as coverage for long-term care.

"That's pie in the sky," said Patricia Combs, a retired junior-high math

teacher from Springboro, Ohio. "It sounds really good, but I don't think

it's attainable … people would complain about their taxes being raised."

Elizabeth Medina of Chicago, an office manager not currently working,

said she worries that quality would slip.

"Overall it sounds terrific," she said. "Yeah! Let's go for it! But

Europe and Canada have their problems with the single-payer system …

it's subpar."

The poll found that 51 percent of initial single-payer backers would

switch to opposition if it took longer for new drugs and treatments to

become available. Only 14 percent would continue to support the plan.

Such an outcome could happen if drugmakers were required to prove that

new medications are therapeutically superior to existing ones. The

current standard is that new drugs be safe and effective.

Additionally, 47 percent of initial supporters would reconsider if

"Medicare for all" meant longer wait times for non-emergency medical

services. That could happen if budget-conscious administrators

encouraged doctors and hospitals to be parsimonious in using high-tech

imaging. Only 18 percent of poll respondents would continue to support

the plan in that case.

Overall, the poll found that health care remains a top issue for

Americans, with three-fourths calling it extremely crucial or very

important.

Topline

HC15. Would you favor or oppose replacing the current private health

insurance system in the United States with a single government-run and

taxpayer-funded plan like Medicare for all Americans that would cover

medical, dental, vision, and long-term care services?

39% Total support

18% Strongly support

21% Somewhat support

26% Neither support nor oppose

33% Total oppose

12% Somewhat oppose

22% Strongly oppose

2% Refused/Not answered

HC15a. Would you support or oppose replacing the health insurance system

in the United States with a single government-run plan if it meant:

Your own taxes would increase

28% Support

32% Neither support nor oppose

29% Oppose

Some people needed to switch doctors

33% Support

37% Neither support nor oppose

29% Oppose

It took longer for new drugs and treatments to become available

14% Support

34% Neither support nor oppose

51% Oppose

Longer wait times for nonemergency medical services

18% Support

35% Neither support nor oppose

47% Oppose

People needed to give up other coverage like employer coverage

28% Support

32% Neither support nor oppose

39% Oppose

The new system would replace Medicare for seniors

37% Support

35% Neither support nor oppose

26% Oppose

http://ap-gfkpoll.com/featured/findings-from-our-latest-poll-32

Topline

http://ap-gfkpoll.com/main/wp-content/uploads/2016/02/AP-GfK_Poll_February-2016-topline_health.pdf

***

Comment by Don McCanne

Most polls place support for a single payer Medicare-for-all national

health program at about 60%, with some variation based on labels,

framing, and polling technique. Yesterday's Kaiser poll placed it at

50%. This new Associated Press GfK poll places it at about 40%, but it

is unusual in that over one-fourth of those polled expressed no

preference. Of those expressing a preference, 54% were supportive and

46% opposed. But there was something else that was also very unusual

about this poll.

Yesterday's Kaiser poll demonstrated that the views on single payer were

malleable. When asked about negative features that allegedly are

associated with single payer, support declined, whereas support

increased when asked about positive features. In this AP-GfK poll they

were asked only about allegedly negative features, and support declined.

But what were these negative features?

* /Your own taxes would increase/ - But no mention was made of the

savings in premiums, out-of-pocket expenses and other taxes that would

more than offset the new taxes, resulting in a net savings.

* /Some people needed to switch doctors/ - But that is a characteristic

of private plans with their narrow networks whereas single payer

provides free choice of health care professionals.

* /It took longer for new drugs and treatments to become available/ -

There is no way that the pharmaceutical industry is going to walk away

from a $3 trillion market.

* /Longer wait times for nonemergency medical services/ - Responsible

stewards would use capacity adjustment and queue management to prevent

excessive queues, as has been done successfully in several other nations.

* /People needed to give up other coverage like employer coverage/ - But

they would be trading that for a superior program with more

comprehensive coverage, reduced out-of-pocket costs and greater choices

in health care.

* /The new system would replace Medicare for seniors/ - Who would want

to continue with the current Medicare program that pays for only about

half of health care when you could have an *improved* Medicare with more

generous benefits?

Why would the Associated Press conduct such a deceptive poll at a risk

of impairing its credibility? When you read the AP release, you can't

help but come to the conclusion that it was designed to slam

presidential candidate Sen. Bernie Sanders and his support of Medicare

for all. They even included a gratuitous comment from an unemployed

office manager to the effect that the single payer system is "subpar"

like in "Europe and Canada" - an absolute falsehood.

Whatever the intentions of the Associated Press, we must make every

effort to dispel the deceptions and disseminate the true facts about

single payer Improved Medicare for All. The health of America is at stake.

Thursday, February 25, 2016

qotd: Lessons from Kaiser poll on single payer

Kaiser Family Foundation

February 25, 2016

Kaiser Health Tracking Poll: February 2016

By Bianca DiJulio, Jamie Firth, Ashley Kirzinger, and Mollyann Brodie

The February Kaiser Health Tracking Poll asked the public about broad

options for changing the health system that are currently being

discussed and finds more Americans (36 percent) say policymakers should

build on the existing law to improve affordability and access to care

than any other option presented. Sixteen percent say they would like to

see the health care law repealed and not replaced, 13 percent say it

should be repealed and replaced with a Republican-sponsored alternative,

and 24 percent say the U.S. should establish guaranteed universal

coverage through a single government plan.

As debate continues over the idea of universal coverage through a single

government plan, the survey finds the public divided, with half saying

they favor the idea and 43 percent saying they oppose it, and some

opinions swayed after hearing counterarguments. In addition, majorities

of Democrats and independents favor the idea, compared to just 20

percent of Republicans. Most Americans think that if guaranteed

universal coverage through a single government plan was put into place,

uninsured and low-income people would be better off, but there is little

consensus among the public about how it would impact their care personally.

This month's poll also explores the public's reaction to a few terms

used to describe the idea of expanding health insurance coverage to all

Americans. Majorities say they have a positive reaction to the terms

"Medicare-for-all" and "guaranteed universal health coverage" and fewer

say the same for "single payer health insurance system" and "socialized

medicine." About half (53 percent) of Democrats say they have a very

positive reaction to "Medicare-for-all" compared with 21 percent who say

the same for "single payer health insurance system."

Next Steps for the Health Care System

While health care ranks fourth as an important voting issue,

presidential hopefuls have proposed a range of visions for the future of

the health care system, from the full repeal of the Affordable Care Act

(ACA) to the adoption of a universal government plan. The survey finds

that when given four broad approaches for the future of the health care

system that are currently being discussed, Americans opinions are split

with the largest share reporting that they favor building on the ACA and

the existing system. Overall, 36 percent say lawmakers should build on

the existing law to improve affordability and access to care, 24 percent

say the U.S. should establish guaranteed universal coverage through a

single government plan, 16 percent say they would like to see the health

care law repealed and not replaced, and 13 percent say it should be

repealed and replaced with Republican-sponsored alternative.

A closer look at views across parties shows that a third of Democrats

(33 percent) favor the idea of universal coverage through a single

government plan but more Democrats (54 percent) say they would prefer to

build on the existing health care law. A roughly similar share of

independents (26 percent) say the U.S. should establish guaranteed

universal coverage through a single government plan, and 36 percent say

lawmakers should build on the existing health care law. The majority of

Republicans (60 percent) say they would like to repeal the health care

law whether it's replaced or not, although 21 percent say they would

like to build on the existing law and 9 percent say they would like

universal coverage through a government plan.

How Malleable are Americans' Opinions of Guaranteed Health Coverage From

a Government Plan?

Although half of the public says they favor having guaranteed health

insurance coverage through a single government health plan, some can be

swayed by counterarguments made by critics. For instance, 20 percent

overall shift their opinion from favor to oppose after hearing that

guaranteed coverage through a single government plan would "require many

Americans to pay more in taxes," 20 percent say they now oppose the idea

after hearing that it would "give the government too much control over

health care," and 14 percent say they now oppose it after hearing that

it would "eliminate or replace the current health care law." On the

other side of the debate, those who originally said they opposed the

idea were also persuaded by arguments, although fewer changed their

opinions after hearing the arguments. About one in 10 changed their

stance from oppose to favor after hearing that guaranteed coverage would

"ensure that all Americans have health insurance as a basic right" (13

percent), that it would "reduce health insurance administrative costs"

(11 percent), and that it would "eliminate all private health insurance

premiums, co-pays, and deductibles paid by employers and individuals"

(11 percent).

Impact of Coverage Through Single Government Plan

Most Americans think that if guaranteed universal coverage through a

single government plan was put into place, uninsured and low-income

people would be better off (60 percent and 57 percent, respectively).

Fewer say that middle class people (34 percent) and people like them (31

percent) would be better off, which is roughly similar to the shares who

say these same groups will be worse of or not be impacted much at all.

Most (63 percent) say it would not have much impact on wealthy people,

just 14 percent say they would be better off and 18 percent say they

would be worse off. Democrats and independents are more likely than

Republicans to report that all people would be better off through a

single government plan.

The country has not had a substantial public debate about single payer

legislation recently and there is little consensus among the public

about how enacting guaranteed universal coverage through a single

government plan would impact their personal health care. Roughly four in

10 say that they think the cost, quality, availability of health care

treatments, and choice of doctors and hospitals would stay about the

same as it is under the current health care system. About a third say

these measures would get worse if universal coverage was put into place

and around two in 10 think these measures would get better. Not

surprising considering their stances on the idea of guaranteed universal

coverage, majorities of Republicans say each measure would likely get

worse if such a plan was enacted, while at least half of Democrats say

each would likely stay about the same. Additionally, those under age 50,

Black and Hispanic Americans, and those with lower incomes are more

likely than their counterparts to say that these measures will get better.

Wording Matters

Politicians and pundits use a variety of terms to describe the idea of

expanding health insurance coverage to all Americans and this month's

poll explores the public's reaction to a few of these terms. Nearly

two-thirds (64 percent) of Americans say they have a positive reaction

to the term "Medicare-for-all" and more than half (57 percent) say they

have a positive reaction to the term "guaranteed universal health

coverage." Less than half of Americans report a positive association

with the phrases "single payer health insurance system" (44 percent) and

"socialized medicine" (38 percent).

Similar to the public at large, more Democrats report having a positive

reaction to "Medicare-for-all" and "guaranteed universal health

coverage" than say the same about "socialized medicine" or "single payer

health insurance system." Additionally, more Democrats have positive

reactions to all of the terms than Republicans and independents do.

Around half of Democrats report a very positive reaction to

"Medicare-for-all" (53 percent) and "guaranteed universal health

coverage" (44 percent), while fewer Republicans say the same for each

(17 percent and 9 percent, respectively). Two in 10 Democrats report

very positive reactions to "socialized medicine" (22 percent) and

"single payer health insurance system" (21 percent), while fewer than

one in 10 Republicans do.

Topline

4. Which of the following comes closest to your view of the future of

the US health care system?

16% The health care law should be repealed and NOT replaced

13% The health care law should be repealed and replaced with a

Republican-sponsored alternative

36% Lawmakers should build on the existing health care law to

improve affordability and access to care

24% The U.S. should establish guaranteed universal coverage through

a single government plan

6% None of these/Something else

4% Don't know/refused

5. Do you favor or oppose having guaranteed health insurance coverage

in which all Americans would get their insurance through a single

government health plan?

50% Favor

27% Strongly favor

23% Somewhat favor

43% Oppose

13% Somewhat oppose

30% Strongly oppose

7% Don't know/Refused

19. I am going to read you a list of terms. Please tell me if you have

a positive or negative reaction to each term.

a. Socialized Medicine

38% Positive

15% Very positive

23% Somewhat positive

49% Negative

19% Somewhat negative

30% Very negative

12% Other

b. Medicare-for-all

64% Positive

36% Very positive

27% Somewhat positive

29% Negative

15% Somewhat negative

14% Very negative

6% Other

c. Single payer health insurance system

44% Positive

15% Very positive

29% Somewhat positive

40% Negative

21% Somewhat negative

19% Very negative

17% Other

d. Guaranteed universal health coverage

57% Positive

28% Very positive

29% Somewhat positive

38% Negative

15% Somewhat negative

22% Very negative

6% Other

Report:

http://kff.org/health-reform/poll-finding/kaiser-health-tracking-poll-february-2016/

Topline:

http://files.kff.org/attachment/topline-methodology-kaiser-health-tracking-poll-february-2016

***

Comment by Don McCanne

About half of Americans would prefer a single government health plan for

everyone, according to this poll. However, when offered several choices,

more would prefer to build on the current system (36%) than would prefer

to establish a single government plan (24%). Also, followup questions

show that the opinions of a single government plan are quite malleable,

depending whether the query has a positive or negative slant.

The malleability of opinion and the poor understanding of the benefits

of single payer demonstrate that the public still has a relatively weak

understanding of precisely what a single payer system is. We need to

intensify our educational efforts.

Perhaps more disconcerting is that more people would prefer to build on

the Affordable Care Act than to establish a single government plan. The

message of the incrementalists seems to be carrying the day. People

believe that we can simply tweak the current system and achieve the same

goals as single payer.

What people haven't grasped are the fundamental differences between the

financing infrastructures of our fragmented multi-payer system and a

well designed single payer system. Recent Quote of the Day messages

describing some of the flaws in our current system have asked the

question, "What incremental change would fix this particular problem?"

The answers don't come easy.

It's easy to say that we can build on the Affordable Care Act by

gradually covering more people and by controlling spending by

eliminating waste, but these are wishes, not policies. In most

instances, there is no simple patch that would work, but rather most

changes increase the administrative complexity, add significantly to the

costs, and fall short of fully correcting the specific problems addressed.

This is a very important message that we have to deliver. Our current

financing infrastructure is not particularly amenable to incremental

patches. It is imperative that we replace our flawed infrastructure with

one that automatically addresses the problems that we still face in

health care financing. Single payer would do that.

This poll also tested labels for a single payer system. Close to

two-thirds had a positive reaction to the term, "Medicare-for-all."

People also had a positive reaction to "guaranteed universal health

coverage," but that doesn't mean much and has been misused as a label

for systems that are neither guaranteed nor universal. Yet people seem

to be split or confused by the term, "single payer health insurance system."

"Medicare-for-all" does seem to be preferred, but some opponents are

quick to point out the deficiencies in our Medicare program. Adding

"improved," as in "Improved Medicare for All," defuses that challenge.

So do not let people get away with saying that we'll simply build on the

system we have. Demand that they define the precise incremental steps

and how each would move us significantly closer to truly affordable care

for absolutely everyone. If you keep pushing them they'll eventually

have to describe a single payer system because patches to our current

system just won't get us there.

Wednesday, February 24, 2016

qotd: ACA reform has not eliminated bad debt for hospitals

Bloomberg Business

February 23, 2016

Bad Debt Is the Pain Hospitals Can't Heal as Patients Don't Pay

By John Lauerman

A type of pain that hospitals thought they had relieved has come back

with a vengeance: it's called bad debt.

Hospitals have long struggled to collect bills when patients aren't

covered by insurance -- creating delinquent accounts. The Affordable

Care Act was supposed to relieve some of that strain by helping pay for

coverage for millions of Americans and expanding Medicaid in some states

to cover the poor.

Yet while millions of people have gained coverage since Obamacare became

law in 2010, there's also been an increase in insurance that comes with

high deductibles and cost-sharing. Under those plans, the first few

thousand dollars of annual medical expenses come out of patients'

wallets. That's money that hospitals like Childress Regional Medical

Center in the Texas Panhandle region are unlikely to collect.

"It feels like a sucker punch," said John Henderson, the nonprofit

hospital's chief executive. "When someone has a really high deductible,

effectively they're still uninsured, and most people in Childress don't

have $5,000 lying around to pay their bills."

The rate of uninsurance in the U.S. has fallen to 9.1 percent from 15.7

percent in 2009. Yet in the first nine months of 2015, about 36 percent

of the U.S. insured were covered by high-deductible or consumer-directed

health plans that can require considerable out-of-pocket payments,

compared with about 25 percent in 2010, according to a CDC survey.

Hospitals are feeling the pressure from those patients. Community Health

Systems Inc. operates 195 hospitals in 29 states and is the U.S.'s

second-biggest for-profit U.S. hospital chain. This month, it revised

its fourth-quarter 2015 provision for bad debt up by $169 million -- and

said that 40 percent, or about $68 million of that amount, was from

patients being unable to pay deductibles and co-payments. Patient

bankruptcies also contributed, the company said.

While higher out-of-pocket charges can lower what insurance costs up

front, it means more costs for patients on the back end. Under

individual Obamacare mid-level "silver" plans, the annual deductible was

$2,556, and under less expensive, low-level "bronze" plans it was $5,328

in 2015, according to the Kaiser Family Foundation.

Outside of Obamacare, deductibles are becoming more common, as well.

Last year, 81 percent of coverage people got through work came with a

deductible, up from 70 percent in 2010, according to Kaiser. The average

deductible in a high-deductible, individual plan gained through work was

$2,099 last year.

Rural hospitals have been hit particularly hard. Minnesota has long had

high rates of care coverage, and many employers have switched to high

deductible offerings, according to Joe Schindler, vice president of

finance for the Minnesota Hospital Association. Last year, bad debt rose

by 20 percent to $425 million at the association's 140 member hospitals.

http://www.bloomberg.com/news/articles/2016-02-23/bad-debt-is-the-pain-hospitals-can-t-heal-as-patients-don-t-pay

***

Comment by Don McCanne

The Affordable Care Act (ACA) was supposed to make health care

affordable, yet many hospitals are finding that patients are generating

more bad debt. A large portion of that is due to the inability of

patients to pay the high deductibles and other cost sharing required by

their insurance plans. Patient bankruptcies also compound the problem.

Deductibles are used by insurers to shift some of the spending to

patients so that the insurers can keep the premiums for their plans

competitive. But much has been written about how these deductibles

create financial burdens for patients. And when the patients cannot pay

the deductibles, physicians and hospitals are faced with bad debt. With

greater use of higher deductibles, the problems with debt will surely

increase.

This is a problem inherent in the model of reform perpetuated by ACA.

Various policies such as the deductibles are developed to comply with

the private insurance model. How would the incrementalists fix this

problem? There are too many moving levers.

What we should have instead is a system in which the policies are

developed to comply with the needs of patients. Deductibles can be

eliminated if we do away with premiums as a means of financing health care.

The financing of a single payer system is not through individual

premiums but rather is through a single universal risk pool that is

funded equitably through progressive taxes, making health care

affordable for everyone. Medical debt simply goes away.

Tuesday, February 23, 2016

qotd: Hillary Clinton resurrects public option, or not?

Politico Pulse

February 23, 2016

Clinton resurrects public option

By Dan Diamond

Hillary Clinton is bringing back the "public option," a liberal health

reform that so far has gotten little attention this campaign cycle as

Bernie Sanders has pushed an even more progressive single-payer plan.

The public option — initially conceived as a government-run alternative

to private insurance — was backed by Clinton in her 2008 campaign and

was the subject of intense debate during the drafting of the Affordable

Care Act. However, Democrats abandoned the measure after Senate

moderates said they wouldn't vote for it because it expanded the

government's role in health care too far.

Clinton is again making clear she supports a version of the public

option. This time, though, she wants to allow states to opt in,

according to a newly updated policy position on her campaign website.

How would it work — and why now?

Clinton appears to be suggesting that states could use the ACA's 1332

waivers to "empower states to establish a public option choice" in 2017.

It's plausible that liberal governors and legislatures would opt in,

while keeping the fight over this progressive idea largely out of

Washington.

It's unclear exactly what Clinton's thinking is on this, however. The

campaign didn't respond to repeated requests from POLITICO to clarify

its new policy language.

Just last month: Clinton said 'we couldn't get the votes' for public option.

While Clinton's spokesperson told PULSE that she has consistently backed

the public option since the 2008 campaign, Clinton pointed out just last

month that Congress wasn't able to get it through during the ACA. "There

was an opportunity to vote for what was called the public option,"

Clinton said during a debate in South Carolina, after she rebuked

Sanders' plan as impractical. "But even when the Democrats were in

charge of Congress, we couldn't get the votes for that."

http://www.politico.com/tipsheets/politico-pulse/2016/02/clinton-resurrects-public-option-califf-nomination-moves-forward-how-the-election-could-shape-the-market-212836

***

Hillary for America

Affordable health care is a basic human right.

Hillary has never given up on the fight for universal coverage—and she

won't stop now. Building on the Affordable Care Act to expand coverage

for millions of Americans, Hillary will:

* Continue to support a "public option" — and work to build on the

Affordable Care Act to make it possible. As she did in her 2008 campaign

health plan, and consistently since then, Hillary supports a "public

option" to reduce costs and broaden the choices of insurance coverage

for every American. To make immediate progress toward that goal, Hillary

will work with interested governors, using current flexibility under the

Affordable Care Act, to empower states to establish a public option choice.

https://www.hillaryclinton.com/issues/health-care/

***

Physicians for a National Health Program

May 26, 2009

Public Plan Option in a Market of Private Plans

By David Himmelstein, M.D. and Steffie Woolhandler, M.D., M.P.H.

The "public plan option" won't work to fix the health care system for

two reasons.

1. It forgoes at least 84 percent of the administrative savings

available through single payer. The public plan option would do nothing

to streamline the administrative tasks (and costs) of hospitals,

physicians offices, and nursing homes, which would still contend with

multiple payers, and hence still need the complex cost tracking and

billing apparatus that drives administrative costs. These unnecessary

provider administrative costs account for the vast majority of

bureaucratic waste. Hence, even if 95 percent of Americans who are

currently privately insured were to join the public plan (and it had

overhead costs at current Medicare levels), the savings on insurance

overhead would amount to only 16 percent of the roughly $400 billion

annually achievable through single payer — not enough to make reform

affordable.

2. A quarter century of experience with public/private competition in

the Medicare program demonstrates that the private plans will not allow

a level playing field. Despite strict regulation, private insurers have

successfully cherry picked healthier seniors, and have exploited

regional health spending differences to their advantage. They have

progressively undermined the public plan — which started as the single

payer for seniors and has now become a funding mechanism for HMOs — and

a place to dump the unprofitably ill. A public plan option does not lead

toward single payer, but toward the segregation of patients, with

profitable ones in private plans and unprofitable ones in the public plan.

http://pnhp.org/blog/2009/03/26/himmelstein-and-woolhandler-on-a-public-plan-option/

Comment by Don McCanne

You remember the public option. During the drafting of the Affordable

Care Act (ACA), efforts were made to include a public option - a

government-run plan that would compete with the private health plans in

the insurance marketplace. If the private plans proved that they could

provide greater value, then they would prevail. If the government could

do a better job, then the public option could expand by demand and

eventually become the single payer for the nation, so supporters believed.

The original concept for the public option was to allow individuals to

buy into the Medicare program instead of purchasing private insurance.

There were some obvious problems. Medicare lacked some important

features required of the private plans such as catastrophic coverage -

establishing a maximum out-of-pocket responsibility of paying for health

care. Also, the existing Medicare pool was composed of the elderly and

those with long term disabilities - expensive groups to insure. The

exorbitant premium that would have to be charged could not be

competitive with the private plans.

It was then decided to establish a new public insurance program that was

designed like the private plans and that would have to follow the same

rules. The insurance industry immediately opposed this since it would be

"unfair" competition considering the government resources backing up the

public plan, and the inherently higher administrative costs that the

private insurers face, not to mention the need to profit from their

operations - profit not being a feature of a publicly-owned insurer.

Several (anti-competitive) features were proposed for the public option

which would give the private insurers a "fair" playing field.

The insurers were still concerned that they could not compete against

even a restricted government plan, and thus they continued to oppose it.

There is a basis for that concern since the private Medicare Advantage

plans are able to "compete" with the traditional Medicare program only

because of the overpayments that are being made to the private plans. If

they were in the same playing field, the private plans would perish.

Nevertheless, the issue of the private option became moot when Sen.

Joseph Lieberman, with no votes to spare, threatened to kill the entire

Affordable Care Act if the public option were included.

We were left with the co-ops as a substitute for the public option. The

co-ops are non-profit organizations in which the insured members are the

owners. Congress, under the Republicans, has refused to provide promised

funds, and half of them have collapsed. They are now being used by

opponents of single payer to "prove" that the government would be

incapable of running a single payer system - an obvious non sequitur.

Since the enactment of ACA there have been endless calls to add a public

option. Single payer failed to gain traction because of the pervasive

meme that single payer was not politically feasible. But if we could

just get a public option, that would automatically evolve into a single

payer system, they said.

Then along came Bernie Sanders. He carried the message that not only was

single payer politically feasible, it was a moral imperative to achieve

health care justice for all.

To the surprise of Hillary Clinton and her campaign staff, Bernie

Sanders came out of nowhere and gained traction carrying the single

payer banner, and, as a result, has become a genuine challenge to her

candidacy.

Hillary Clinton has always been an opponent of single payer and instead

has supported the private insurance industry. Some have misinterpreted a

statement of hers many years ago as supporting the fact that we would

have single payer in the United States. But that statement was not in

support of single payer but rather was her threat to us that if we did

not accept her managed competition model of reform, we would have single

payer.

So what was her campaign to do? They decided to bring back the concept

of a public option to appease those who were turning to Sanders because

of his advocacy of single payer. They are relying on the meme that the

public option is our door to single payer (even though it is not true).

But look at what her version of the public option is.

She says we should build on ACA. She has proposed no new federal public

option legislation but she is merely suggesting that the states look at

Sec 1332 of ACA which authorizes waivers for limited innovations on a

state level. Imagine the difficulties that states would have, within the

confines of Sec 1332, in building their own intra-state public plan.

Unless they used private insurance innovations such as high deductibles,

narrow provider networks, and tiered services, the premiums would be

unaffordable to most. A single payer system would be funded equitably

through progressive taxes, but you could not do that with a public

option since that is only one plan in a multi-payer system.

In 2009, David Himmelstein and Steffie Woolhandler explained in very

brief terms why the public option is a flawed concept (reproduced

above). Hillary Clinton is now showing us how it is a diversion from the

reform we really need - single payer. It is up to us, the people, to

convince our politicians that single payer is what we want. It will not

happen without us.

/Physicians for a National Health Program (PNHP) is a nonpartisan

educational organization. It neither supports nor opposes any candidates

for public office./

/

/

Monday, February 22, 2016

qotd: Gov. Pence insists on consumer-driven principles for low-income patients

Indianapolis Star

February 21, 2016

Pence seeking help from Congress in Medicaid dispute

By Maureen Groppe

Gov. Mike Pence wants Congress to get involved in his dispute with the

Obama administration over the evaluation of Indiana's alternative

Medicaid program.

Pence has accused the administration of hiring an evaluator that is

biased against Indiana's approach.

Indiana is one of a handful of states that received permission to not

follow some federal rules when expanding Medicaid coverage under the

Affordable Care Act.

One of the conditions of such waivers is that the demonstration program

be evaluated to see whether it's meeting the expected result. Indiana

must submit an interim evaluation of the program by mid-2016.

For example, Indiana is testing whether requiring participants to make

monthly contributions to a health account that can be rolled over if not

used for health care reduces the use of unnecessary care.

That feature is based on high-deductible insurance plans with health

savings accounts that are becoming increasingly common in private

insurance coverage.

Pence argues that the Urban Institute, one of the evaluators chosen by

the federal government to assess Indiana's plan, has previously been

skeptical of using the health savings account model for Medicaid recipients.

Pence wrote Health and Human Services Secretary Sylvia Burwell in

December, asking that the federal review be dropped as the Healthy

Indiana Plan has already been evaluated by a state-hired contractor.

In a Feb. 10 response, Burwell said the federal evaluation will not

duplicate the state's analysis, and a rigorous evaluation will help the

federal government determine whether other states should be allowed to

use Indiana's model.

Pence said he is "wholly unsatisfied" with that response, and will ask

the GOP-controlled Congress to review the agency's vendor selection process.

While Pence said Burwell always worked in good faith with him while they

negotiated the terms of Indiana's alternative program, there are people

"deep in the bureaucracy" who are "very antagonist towards consumer

driven health care."

"The administration wanted Indiana — and still wants every state — to

just expand traditional Medicaid," he said. "We have the most

significant Medicaid reform in the 50-year history of the program, and

it's working."

A coalition of health care and other advocacy groups wrote a letter last

month in support of the federal government's evaluation of HIP 2.0. The

coalition — which includes Families USA, the March of Dimes and the

American Cancer Society Cancer Action Network — said there can be a

conflict of interest with state-contracted evaluations.

"When a state pays an organization to assess the merits of its own

program there is the potential that the evaluator's objectivity will be

compromised," the coalition wrote to the director of the Center for

Medicaid and CHIP Services.

The groups said aspects of Indiana's program are potentially harmful to

beneficiaries and need to be evaluated before the federal government

decides whether other states can adopt them. Those features include the

option of charging monthly payments to recipients below the poverty

line, blocking coverage for those above poverty who miss their monthly

payments, and the overall complexity of HIP 2.0.

http://www.indystar.com/story/news/2016/02/20/pence-seeking-help-congress-medicaid-dispute/80663058/

The RWJF/Urban Institute report that Pence argues shows a bias against

using healthy savings accounts in Medicaid:

http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2015/rwjf420603

***

Comment by Don McCanne

Gov. Mike Pence of Indiana wants to select his own facts for a report to

CMS confirming that their consumer-directed health program for Medicaid,

authorized by a Sec. 1115 waiver, is meeting Medicaid requirements for

the patients.

They have already independently contracted with the Lewin Group to

provide a report to CMS, but numerous organizations have expressed the

concern that this report could be biased because of the conflict of

interest. CMS has contracted with the Urban Institute, but Gov. Pence

objects because Urban has produced a previous report expressing some

concerns about the option to charge premiums for individuals living in

poverty and about the administrative costs and inefficiencies of health

savings accounts that are used in Indiana's program. Also there is

concern about Medicaid patients being locked out of care if they are in

arrears with their premium payments.

Indiana's program is driven by ideology rather than by objective

application of health policy principles. Pence touts their success at

"applying consumer-health care principles to the Medicaid population."

It is more important for him to require patients to demonstrate

individual responsibility through sharing in the costs of care than it

is to ensure that they do receive the care that they need. It has been

demonstrated that requiring payments creates barriers to care,

particularly for low-income individuals.

Imagine instead having one national standard program that automatically

includes everyone, gives them free choice of their health care

professionals, and removes financial barriers to care. We could have

that with a single payer national health program, as long as we keep

ideologues like Pence out of the way.

Friday, February 19, 2016

qotd: CMS will likely continue to overpay Medicare Advantage plans

Center on Budget and Policy Priorities

February 16, 2016

Making Medicare Advantage Payments More Accurate

By Edwin Park

Anticipating the Centers for Medicare and Medicaid Services' (CMS)

expected announcement Friday of preliminary payment rates and policies

for Medicare Advantage insurers in 2017, insurers have pushed for

changes to the "risk adjustment" system — which raises or lowers

payments to plans based on their enrollees' health. Insurers claim the

system undercompensates them for high-cost enrollees with chronic

conditions. We favor making the system as accurate as possible, but

that should include reducing overpayments to insurers as well.

To be sure, risk adjustment tends to underpredict health spending for

high-cost individuals in poorer health. The Medicare Payment Advisory

Commission (MedPAC) suggests that CMS make several changes to better

account for higher spending by people with multiple chronic conditions

and low-income beneficiaries eligible for both Medicare and Medicaid.

But Medicare Advantage risk adjustment also overcompensates insurers for

healthier, low-cost enrollees. For example, Avalere Health research,

which insurers have cited favorably, shows risk adjustment

overpredicting spending among people with no chronic conditions by 26.9

percent and among people with one or two chronic conditions by 5.1

percent. That's critical because Medicare Advantage enrollees are

healthier than those in traditional Medicare, on average.

CMS could reduce Medicare Advantage overpayments by doing more to

address "upcoding," which the Congressional Budget Office, the

Government Accountability Office (GAO), and academic research cite as a

long-standing problem. The risk adjustment system measures enrollees'

health using a "risk score" based on patient diagnoses; upcoding occurs

when the risk scores that plans submit for their enrollees rise over

time — making enrollees appear increasingly unhealthy — without actual

changes in their health.

Risk scores have risen 9 percent faster in Medicare Advantage, on

average, than in traditional Medicare for comparable beneficiaries,

MedPAC estimates. This leads to excessive payments to Medicare

Advantage plans.

To compensate for upcoding, health reform requires CMS to adjust

Medicare Advantage's risk adjustment system by at least a minimum amount

each year. CMS has only applied the minimum required adjustment in

recent years. A larger adjustment, which MedPAC believes is warranted,

would reduce overpayments to Medicare Advantage plans.

CMS could also reduce upcoding by excluding health assessments from risk

score calculations unless they're later confirmed in treatment settings,

as MedPAC will likely recommend in its March report to Congress.

Medicare Advantage plans increasingly provide health assessments of

their enrollees; for example, a nurse may come to a patient's home to do

a physical exam. CMS has found that some insurers mainly use these

assessments to "collect" diagnoses in order to raise enrollees' risk

scores for purposes of risk adjustment, rather than to improve follow-up

care or identify illnesses requiring treatment. In fact, CMS had

proposed excluding these kinds of assessments but dropped this change in

the face of industry opposition.

http://www.cbpp.org/blog/making-medicare-advantage-payments-more-accurate

***

CMS.gov

February 19, 2016

2017 Medicare Advantage and Part D Advance Notice and Draft Call Letter

Today, CMS released proposed updates to the Medicare Advantage (MA) and

Part D programs through the 2017 Advance Notice and Draft Call Letter.

Through these policies, CMS is proposing updates to the program designed

to improve the accuracy of payments to plans serving beneficiaries who

are dually eligible for Medicare and Medicaid.

CMS is proposing updates to the Risk Adjustment Model used to calculate

payments to Medicare Advantage plans and to the Star Rating system used

to evaluate plan performance. In both cases, the updates reflect a

public process through which CMS shared research findings and solicited

public comment.

Expected Average Change in Revenue: 3.55%

Risk Adjustment Model

CMS is proposing to implement a new Risk Adjustment Model for 2017. The

proposed new model has separate coefficients for partial benefit dually

eligible beneficiaries, full benefit dually eligible beneficiaries, and

non-dually eligible beneficiaries. These proposed changes will improve

the precision of the payments made to plans, including increases in

payments for plans serving full benefit dually eligible beneficiaries.

Coding Pattern Adjustment

Each year, as required by law, CMS makes an adjustment to plan payments

to reflect differences in diagnosis coding between Medicare Advantage

organizations and fee-for-service (FFS) providers. In CY 2017, CMS

proposes to make an adjustment reflective of the statutory minimum.

Using Encounter Data

CMS calculates risk scores using diagnoses submitted by FFS providers

and by Medicare Advantage organizations. Historically, CMS has used

Medicare Advantage diagnoses submitted into CMS' Risk Adjustment

Processing System (RAPS). In recent years, CMS began collecting

encounter data from MA organizations to develop more accurate payment

models. In 2016, CMS began using diagnoses from encounter data to

calculate risk scores, by blending encounter data-based risk scores with

RAPS-based risk scores. In 2017, CMS is proposing to continue using a

blend, using a higher percentage of encounter data-based risk scores.

Star Ratings – Adjusting for Socioeconomic Status

CMS is proposing to implement a new analytical adjustment for a subset

of Star Rating measures that is meant to adjust for plans serving dually

eligible enrollees and/or enrollees receiving the low income subsidy, as

well as enrollees with disabilities. Through this interim adjustment,

CMS seeks to more accurately capture true plan performance, while work

continues by the HHS Assistant Secretary for Planning and Evaluation

(ASPE) and measure stewards in this important area.

https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact-sheets/2016-Fact-sheets-items/2016-02-19.html

CMS Advance Notice of Methodological Changes for Calendar Year (CY) 2017

for Medicare Advantage (MA) Capitation Rates, Part C and Part D Payment

Policies and 2017 Call Letter (over 220 pages):

https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Downloads/Advance2017.pdf

***

AHIP

January 28, 2016

AHIP, Coalition for Medicare Choices Launch Nationwide Ad and Grassroots

Campaign to Protect Medicare Advantage

As CMS prepares to release proposed Medicare Advantage payment policies,

AHIP's Coalition for Medicare Choices (CMC) is launching a

coast-to-coast mobilization of its 2 million Medicare Advantage

beneficiaries who are calling on Washington to protect their coverage

from further cuts.

"Medicare Advantage is the game-changer. It's the foundation for

innovative, high-quality care delivery that seniors and the country

demand," AHIP President and CEO Marilyn Tavenner said. "CMS should

protect millions of beneficiaries who depend on Medicare Advantage and

strengthen -- not undermine -- the program moving forward."

https://www.ahip.org/News/Press-Room/2016/AHIP,-Coalition-for-Medicare-Choices-Launch-Nationwide-Ad-and-Grassroots-Campaign-to-Protect-Medicare-Advantage.aspx

***

Comment by Don McCanne

Today CMS released proposed updates for the 2017 Medicare Advantage (MA)

plans. It appears that, once again, CMS will be co-conspirators with the

insurance industry in increasing net MA payment rates when the

Affordable Care Act requires reduction of the MA overpayments.

The Medicare Payment Advisory Commission (MedPAC) has recommended that

CMS apply a larger adjustment to the MA risk adjustment system to reduce

overpayments to the MA plans. Yet, once again, as with prior years, CMS

is making "an adjustment reflective of the statutory minimum."

Another example is that the MA plans have been using "encounter data" to

upcode the diagnoses of the MA patients. Home visits are made, not by

the health care providers but by representatives of the MA insurance

plans, in order to find other disorders that can be used to pad the

diagnostic list, making these patients appear sicker than they really

are, thus qualifying the MA plans for higher payments than warranted.

MedPAC is expected to recommend excluding encounter data from risk score

calculations unless they are later confirmed in treatment settings. Yet,

CMS is instead proposing to use a higher percentage of encounter

data-based risk scores.

Instead of a reduction in payments, CMS is proposing a 3.55% increase.

CMS invites comments through March 4, 2016 before the final publication

on April 4, 2016. During that time, AHIP, the insurance lobby

organization, will be negotiating with CMS for further adjustments that

will favor the MA plans. Each year that has resulted in additional

innovative chicanery that further thwarts the intent of ACA to reduce MA

overpayments. Since the new President and CEO of AHIP is Marilyn

Tavenner, the former Administrator of CMS, it is anticipated that the

negotiations on behalf of the MA plans will be quite successful.

Ensuring success of the MA plans is part of the plot to eventually

privatize Medicare - converting it into a premium support system

(vouchers) for a market of private plans that will displace the

traditional Medicare program. The value of the voucher equivalents will

erode with time, shifting ever more of the costs to the Medicare

beneficiaries. It will be disastrous.

By this time it was expected that MA plan enrollment would begin to

decline since the private insurance industry is incapable of providing

comparable benefits at the same or lower costs than traditional

Medicare, because their administrative costs are significantly higher

than those of the traditional program, plus they need to return a profit

to their investors. They have been profitable only because they have

continued to be successful in enrolling healthier, less costly patients

while at the same time receiving overpayments from the government.

Thus this conspiracy reenacted each year to use innovative payment

schemes (chicanery) is vital to this industry. Members of AHIP's

Coalition for Medicare Choices will, once again, pressure members of

Congress to cajole CMS into "saving" the Medicare Advantage plans

through whatever accounting tools they can find (all with a wink and a

nod). What is surprising is that this has not provoked the outrage of

taxpayers. But maybe this is not so surprising after all since hardly

anyone recognizes the terrible crime that is taking place before our

very eyes.

Thursday, February 18, 2016

qotd: Return on investment in health care

The New England Journal of Medicine

February 18, 2016

Asymmetric Thinking about Return on Investment

By David A. Asch, M.D., Mark V. Pauly, Ph.D., and Ralph W. Muller, M.A.

Lately, we've attended many conferences about providing health care to

patients with high medical and social needs — people with chronic

illnesses who are frequently readmitted to the hospital. It seems as if

every presentation refers to "return on investment" (ROI), which is

invariably presented as a constraint — as in "Our program kept people

out of the hospital, but we just couldn't get the ROI to work." Heads

nod understandingly, and then participants move on to other topics.

At conferences about providing care for patients with cancer or other

acute illnesses, by contrast, we almost never hear the term ROI.

Instead, people talk about clinical gains, using understandable and

patient-centered terms like "survival." Though high drug prices are

sometimes mentioned, no one ever says the ROI is prohibitive. No one

mentions ROI at all.

There is no obvious reason why ROI is more relevant to some clinical

situations than to others. So why do we focus so heavily on ROI when the

topic is chronic illness but rarely mention it when the topic is cancer?

A huge amount of the cancer care we deliver provides such small personal

and social gains that, were those gains monetized, the endeavor's ROI

would be deeply negative. And yet we ask, "What's the ROI of that

program that keeps chronically ill patients out of the hospital?" but

not "What's the ROI of treating advanced lung cancer?"

Providing cancer care and averting hospitalizations are financed

differently. It's hard to create a favorable ROI for reducing volume in

a system dominated by fee-for-service payments for delivering care.

Sometimes a favorable ROI is achieved passively when, for example,

avoiding care frees up capacity for patients whose care is more

profitable. More actively, the avoidance of care can be financed by

establishing punishments for delivering avoidable care (penalties for

readmissions, for example) or by shifting its cost to the providers

themselves (e.g., through capitated or bundled payments).

It might seem that we could make the ROI for appropriate care more

favorable if we imposed higher penalties on inappropriate care, just as

we could make the ROI for treating cancer less favorable by paying less

for cancer treatments. Despite that apparent symmetry, the choice of

financing mechanisms — payments versus penalties — determines how much a

health care goal will be advanced. If the ROI didn't work for some form

of cancer care — because the payment received was lower than the cost

incurred — doctors and hospitals would almost certainly argue for higher

payments. But when the ROI doesn't work for keeping challenging patients

with chronic disease out of the hospital, it's implausible that doctors

or hospitals will plead for increased readmission penalties. There isn't

any mathematical reason to prefer payment in the form of rewards over

payment in the form of avoided penalties, but you can typically generate

more advocates for your cause by paying people to follow you than by

penalizing them for going the other way.

So when advocates and organizations devoted to keeping people out of the

hospital lament their inability to make the ROI work, they should know

that the game is rigged against them. In the highly regulated context of

health care, the amount and structure of financing are chosen rather

than preordained. The ROI is favorable or unfavorable not because of the

workings of some invisible hand, but because of choices someone —

usually a private or public insurer — has made regarding what amounts

will be paid for various types of care and what form payments will take.

What if the financing of cancer care and of efforts to achieve

population health goals traded places? Suppose doctors and hospitals

were paid for cancer care by capitation or bundles or through penalties

for undesired outcomes and were paid directly and adequately to keep

people out of the hospital. Oncologists might begin lamenting that

although new approaches to cancer care helped patients, they just

couldn't get the ROI to work. And the outlook for population health

might become less financially gloomy.

Rewards and penalties have the same ultimate effect on investment

income, but they influence thinking in different ways. We might

encourage greater effort and innovation in keeping people out of the

hospital and coordinating care if we reframed its financing as positive

payments for noble work rather than punitive revenue reductions. As U.S.

health care financing begins again to shift risks to hospitals and

physicians through bundled payments or readmission penalties, the

financing of the care for our most challenging patients might be better

shifted in the other direction.

http://www.nejm.org/doi/full/10.1056/NEJMp1512297

***

Comment by Don McCanne

The concept of return on investment (ROI) in health care may represent

what is wrong with our system that causes it to be so expensive yet

often mediocre by international standards.

Most health care professionals and institutions are largely fixated on

their efforts to provide the best patient care they can with the given

resources. But much of the medical-industrial complex is fixated on ROI,

as is obvious by the examples of the private, for-profit insurers and

the pharmaceutical firms with their egregiously high profits.

The authors of this article discuss trying to take care of cancer

patients in which ROI standards are not considered since "monetized"

gains for cancer patients would be "deeply negative." They contrast that

with readmissions of patients with chronic illnesses in which the ROI is

important based on the penalties assessed for failing to prevent the

readmissions.

On the one hand, the professionals and institutions are simply paid for

providing appropriate care. On the other, attempting to provide

appropriate care is complicated by a necessity to consider the potential

of a negative ROI because of financial considerations - penalties -

which have nothing to do with the actual medical care being provided.

Instead of ROI driving motivation, the authors suggest that we reframe

health care financing as "positive payments for noble work rather than

punitive revenue reductions."

They conclude, "As U.S. health care financing begins again to shift

risks to hospitals and physicians through bundled payments or

readmission penalties, the financing of the care for our most

challenging patients might be better shifted in the other direction."

Noble provision of health care services - a prime goal of a single payer

national health program.

qotd: Return on investment in health care

The New England Journal of Medicine

February 18, 2016

Asymmetric Thinking about Return on Investment

By David A. Asch, M.D., Mark V. Pauly, Ph.D., and Ralph W. Muller, M.A.

Lately, we've attended many conferences about providing health care to

patients with high medical and social needs — people with chronic

illnesses who are frequently readmitted to the hospital. It seems as if

every presentation refers to "return on investment" (ROI), which is

invariably presented as a constraint — as in "Our program kept people

out of the hospital, but we just couldn't get the ROI to work." Heads

nod understandingly, and then participants move on to other topics.

At conferences about providing care for patients with cancer or other

acute illnesses, by contrast, we almost never hear the term ROI.

Instead, people talk about clinical gains, using understandable and

patient-centered terms like "survival." Though high drug prices are

sometimes mentioned, no one ever says the ROI is prohibitive. No one

mentions ROI at all.

There is no obvious reason why ROI is more relevant to some clinical

situations than to others. So why do we focus so heavily on ROI when the

topic is chronic illness but rarely mention it when the topic is cancer?

A huge amount of the cancer care we deliver provides such small personal

and social gains that, were those gains monetized, the endeavor's ROI

would be deeply negative. And yet we ask, "What's the ROI of that

program that keeps chronically ill patients out of the hospital?" but

not "What's the ROI of treating advanced lung cancer?"

Providing cancer care and averting hospitalizations are financed

differently. It's hard to create a favorable ROI for reducing volume in

a system dominated by fee-for-service payments for delivering care.

Sometimes a favorable ROI is achieved passively when, for example,

avoiding care frees up capacity for patients whose care is more

profitable. More actively, the avoidance of care can be financed by

establishing punishments for delivering avoidable care (penalties for

readmissions, for example) or by shifting its cost to the providers

themselves (e.g., through capitated or bundled payments).

It might seem that we could make the ROI for appropriate care more

favorable if we imposed higher penalties on inappropriate care, just as

we could make the ROI for treating cancer less favorable by paying less

for cancer treatments. Despite that apparent symmetry, the choice of

financing mechanisms — payments versus penalties — determines how much a

health care goal will be advanced. If the ROI didn't work for some form

of cancer care — because the payment received was lower than the cost

incurred — doctors and hospitals would almost certainly argue for higher

payments. But when the ROI doesn't work for keeping challenging patients

with chronic disease out of the hospital, it's implausible that doctors

or hospitals will plead for increased readmission penalties. There isn't

any mathematical reason to prefer payment in the form of rewards over

payment in the form of avoided penalties, but you can typically generate

more advocates for your cause by paying people to follow you than by

penalizing them for going the other way.

So when advocates and organizations devoted to keeping people out of the

hospital lament their inability to make the ROI work, they should know

that the game is rigged against them. In the highly regulated context of

health care, the amount and structure of financing are chosen rather

than preordained. The ROI is favorable or unfavorable not because of the

workings of some invisible hand, but because of choices someone —

usually a private or public insurer — has made regarding what amounts

will be paid for various types of care and what form payments will take.

What if the financing of cancer care and of efforts to achieve

population health goals traded places? Suppose doctors and hospitals

were paid for cancer care by capitation or bundles or through penalties

for undesired outcomes and were paid directly and adequately to keep

people out of the hospital. Oncologists might begin lamenting that

although new approaches to cancer care helped patients, they just

couldn't get the ROI to work. And the outlook for population health

might become less financially gloomy.

Rewards and penalties have the same ultimate effect on investment

income, but they influence thinking in different ways. We might

encourage greater effort and innovation in keeping people out of the

hospital and coordinating care if we reframed its financing as positive

payments for noble work rather than punitive revenue reductions. As U.S.

health care financing begins again to shift risks to hospitals and

physicians through bundled payments or readmission penalties, the

financing of the care for our most challenging patients might be better

shifted in the other direction.

http://www.nejm.org/doi/full/10.1056/NEJMp1512297

***

Comment by Don McCanne

The concept of return on investment (ROI) in health care may represent

what is wrong with our system that causes it to be so expensive yet

often mediocre by international standards.

Most health care professionals and institutions are largely fixated on

their efforts to provide the best patient care they can with the given

resources. But much of the medical-industrial complex is fixated on ROI,

as is obvious by the examples of the private, for-profit insurers and

the pharmaceutical firms with their egregiously high profits.

The authors of this article discuss trying to take care of cancer

patients in which ROI standards are not considered since "monetized"

gains for cancer patients would be "deeply negative." They contrast that

with readmissions of patients with chronic illnesses in which the ROI is

important based on the penalties assessed for failing to prevent the

readmissions.

On the one hand, the professionals and institutions are simply paid for

providing appropriate care. On the other, attempting to provide

appropriate care is complicated by a necessity to consider the potential

of a negative ROI because of financial considerations - penalties -

which have nothing to do with the actual medical care being provided.

Instead of ROI driving motivation, the authors suggest that we reframe

health care financing as "positive payments for noble work rather than

punitive revenue reductions."

They conclude, "As U.S. health care financing begins again to shift

risks to hospitals and physicians through bundled payments or

readmission penalties, the financing of the care for our most

challenging patients might be better shifted in the other direction."

Noble provision of health care services - a prime goal of a single payer

national health program.

Wednesday, February 17, 2016

qotd: Link to today's Quote of the Day

Link to Huffington Post article, "Medicare's History Belies Claim That

Medicare-for-All Would Disrupt Care":

http://www.huffingtonpost.com/steffie-woolhandler/medicares-history-belies-_b_9245484.html

qotd: Medicare's History Belies Claim That Medicare-for-All Would Disrupt Care

The Huffington Post

February 16, 2016

Medicare's History Belies Claim That Medicare-for-All Would Disrupt Care

By Steffie Woolhandler and David Himmelstein

ASSOCIATED PRESS

*It Disrupted Jim Crow, but Otherwise the Transition Was Smooth*

Hillary Clinton and others charge that Bernie Sanders' Medicare-for-All

plan would disrupt and threaten Americans' health care. But the smooth

rollout of Medicare-for-Seniors in 1965 -- which many had also predicted

would bring chaos -- belies that charge.

Medicare, signed into law on July 30, 1965, went live just 11 months

later. By then, 18.9 million seniors had signed up, 99 percent of those

eligible.

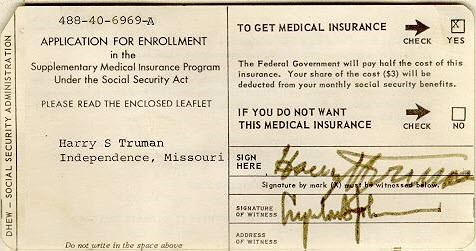

To accomplish this feat (largely without computers) the Social Security

Administration mailed an information leaflet and sign-up cards

<https://www.ssa.gov/history/ssa/lbjmedicare3.html> preprinted with each

individual's name and Social Security number (see example below) to

seniors on the Social Security and railroad retirement rolls, as well as

Civil Service annuitants and a million other seniors identified through

IRS records.

2016-02-16-1455651003-9836566-Medicareenrollmentcard.jpg

<http://images.huffingtonpost.com/2016-02-16-1455651003-9836566-Medicareenrollmentcard.jpg>

{kind=link}

Image: Social Security Administration History Archives

To contact hard-to-reach seniors, the federal government reached out to